The first quarter of 2026 was a reminder that market leadership can change quickly. After U.S. stocks powered through a long list of headline risks in 2025, investors entered the new year confronting a more difficult mix of falling large-cap growth stocks, persistent inflation concerns, rising bond yields, and renewed geopolitical tensions. By quarter-end, the S&P 500 had posted its worst quarterly decline since 2022, while the tech-heavy Nasdaq was hit even harder. In short, the market environment became meaningfully more complex as the quarter progressed.

Importantly, many of the pressure points we highlighted heading into the year did not disappear. They simply evolved. The concentration risk embedded in the largest U.S. technology stocks became more visible. The Federal Reserve’s balancing act became more difficult. And by late March, a sharp rise in oil prices tied to the expanding conflict in the Middle East added another layer of uncertainty for both the economy and financial markets. The result was a quarter that tested investor confidence after an extended period of resilience.

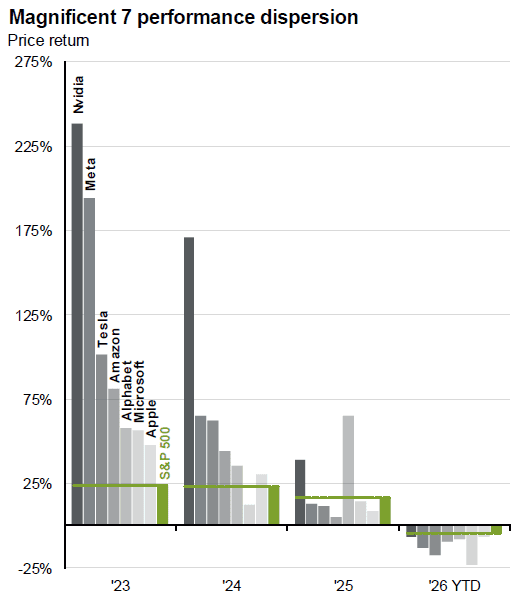

Magnificent 7

In January, we noted that the “Magnificent 7” stocks – Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla – would remain a key market theme in 2026, given their outsized weighting in the S&P 500 and elevated valuations. That view was quickly reinforced in the first quarter, as all seven stocks posted negative returns. After previously driving market gains, the Magnificent 7 became a meaningful drag on broader equity performance.

Source: JPMorgan

This pullback does not invalidate the longer-term case for artificial intelligence – a key driver of the prior gains – or for the businesses involved. It does, however, emphasize an important point: when leadership becomes highly concentrated and valuations extended, even a modest change in sentiment can have an outsized impact on the broader market.

As we have discussed before, elevated valuations are not automatically a problem. But they do leave less room for disappointment. Investors have spent the past several years rewarding companies tied to AI infrastructure, AI services, and AI-enabled products. In the first quarter, the market appeared to take a more discerning view, asking tougher questions about spending levels, earnings durability, and how quickly those investments will translate into lasting returns. We continue to believe these companies are important, but the quarter served as a useful reminder that diversification matters – especially when so much of index performance has been driven by a small group of stocks.

The Fed’s Balancing Act

Another familiar theme this past quarter was the Federal Reserve. At its March meeting, the Fed noted that economic activity continued to expand at a solid pace, while job gains had moderated and inflation remained somewhat elevated. That characterization neatly captures the challenge facing policymakers: growth has not rolled over, but the labor market has clearly lost momentum, and inflation has yet to return to the Fed’s desired target.

The March employment report reflected that same tension. The unemployment rate edged down to 4.3%, but wage growth moderated, hiring softened, and sizable revisions to prior months underscored ongoing labor market volatility. While these developments do not point to immediate weakness, they suggest a thinner margin of safety than investors have enjoyed in recent years. At the same time, inflation data through March indicate that price pressures remain a concern. This is precisely the kind of backdrop that complicates the task for the Fed: policymakers cannot confidently declare victory on inflation, yet they also cannot ignore emerging signs of softness in the labor market.

The bond market reflected that uncertainty. Earlier in the quarter, investors were still focused on the possibility of Fed easing. By late March, however, rising energy prices and inflation worries had pushed Treasury yields higher and reduced confidence around rate cuts. In other words, the market began to worry that the Fed may have less flexibility than many had assumed coming into the year.

Geopolitics, Energy, and Volatility

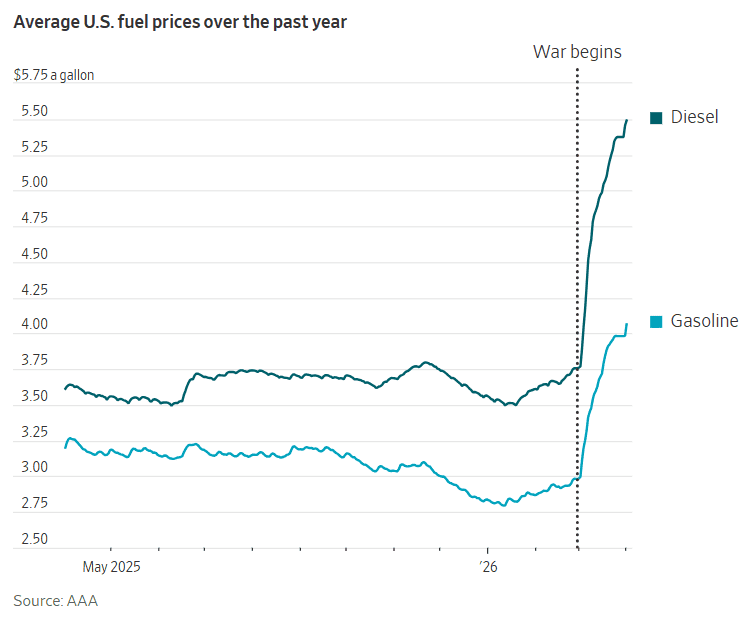

Late in the quarter, geopolitical developments added another layer of complexity to an already challenging backdrop. The expanding conflict involving Iran drove a sharp spike in oil prices and reintroduced stagflation concerns into the market narrative – namely, the risk of slower growth alongside higher inflation. This combination is particularly difficult for markets, as it tends to pressure both equities and fixed income simultaneously.

One way to think about this dynamic is through rising gasoline prices. As consumers spend more at the pump, they have less discretionary income to allocate elsewhere, which can weigh on corporate earnings. At the same time, higher fuel costs raise transportation expenses, feeding through to the price of a wide range of goods.

Source: Wall Street Journal

As we have said in the past, most geopolitical events are difficult to treat as directly investable for long-term investors. They are important to monitor from a risk-management standpoint, but they rarely provide a durable roadmap for portfolio changes on their own. What makes this episode more relevant is the way it feeds into other market variables – namely oil, inflation expectations, Treasury yields, and Federal Reserve policy. These are the channels through which geopolitical developments can materially impact markets, adding complexity to the overall investment landscape.

A Note on Diversification

If there is one encouraging takeaway from the first quarter, it is that 2026 is once again reinforcing the value of diversification. The biggest winners of the prior cycle did not lead this quarter, and a market built so heavily around a narrow group of U.S. mega cap stocks became more vulnerable once that leadership faltered. Environments like this are exactly where a diversified portfolio can prove its worth. For example, international stocks and gold once again outperformed during the quarter.

That does not mean every diversified asset class will work all the time, or that the quarter was easy across the board. It does mean that investors are being reminded, yet again, why we place such emphasis on broad diversification, thoughtful asset allocation, and a long-term perspective tied to your financial plan. When markets become more concentrated, more headline-driven, and more sensitive to policy and geopolitical developments, reacting emotionally tends to be the least productive response. Discipline remains the better approach.

The year is still young, and many of the key themes we entered 2026 watching remain unresolved. We will continue to monitor the path of inflation, labor market trends, Federal Reserve policy, developments in the Middle East, and the durability of earnings growth across both U.S. and international markets. At the same time, our core playbook remains unchanged. We will avoid overreacting to short-term noise, continue rebalancing prudently where appropriate, and keep portfolios aligned with the objectives that matter most to you.

As always, our advisory team is here to answer any questions you may have.